Short Term health insurance illegal in Illinois as of 01/01/2025

ON July 10, 2024, Illinois Governor J.B. Pritzker signed HB2499 into law. That law known as Public Act 103-0649 rendered all Short Term policies illegal for sale in the state of Illinois as of January 1, 2025.

SHORT TERM HEALTH INSURANCE LIMITED TO 3 MONTHS IN DURATION NATIONWIDE AS OF 09/01/2024.

On March 28, 2024, HHS – Health & Human Services published this finalized rule authored by the former Biden administration. This rule limits all Short Term health insurance policies to no more than 3 months in duration. Worse yet, the rule prohibits the ability to purchase another 3 month policy from the same insurer after the first 3 month policy ends. This being the case, Short Term policies are no longer safe to purchase in any state after September 1, 2024 unless you need the coverage for only the last 3 months of a calendar year.

SHORT TERM HEALTH INSURANCE FROM UNITED HEALTHCARE AND ALLSTATE INSURANCE COMPANIES

If you live outside of the state of Illinois and need Short Term health insurance for less than 3 months. United Healthcare’s Short Term policies are the most comprehensive non ACA-qualified Short Term health insurance policies available. Unlike other Short Term policies, these policies cover outpatient prescription drugs and your health plan deductible is waived for Urgent Care visits. United Healthcare also covers each insured member to $2,000,000. United Healthcare’s Short Term policies also include their national “Choice Plus” PPO network which includes in network access to Chicago’s Teaching hospitals such as Northwestern Memorial, University of Chicago, Rush university medical center and the Lurie Children’s hospital. You can search for in network PPO providers within United Healthcare’s Choice Plus PPO by clicking here. United Healthcare’s best designed plan is their “Short Term Medical Plus Elite” plan which provides 100% coverage after the deductible has been satisfied. It also provides a “first dollar” (no deductible required) benefit for outpatient Urgent Care visits. For quotes and to apply online click the United Healthcare logo below.

The second best priced and best designed Short Term health insurance policies are available from Allstate Health Solutions. Their Enhanced Short Term policies cover each insured member up to $1,000,000. Allstate’s Short Term policies also include a national PPO network. That network is Aetna’s Open Choice PPO network. It also includes in network access to Chicago’s Teaching hospitals including Northwestern Memorial, University of Chicago medica center, Rush university medical center and Lurie Children’s hospital. You can search for in network providers PPO providers within Aetna’s Open Choice PPO network by clicking here. For quotes and to apply online click the Allstate Health Solutions logo below:

![]()

PLEASE NOTE: There are two other health insurance carriers offering Short Term health insurance policies in the state of Illinois. They are Independence American via IHC – Independence Holding Group and “Pivot Health” products via Companion Life insurance company. These carriers offer Indemnity policies on a Short Term basis. Indemnity policies do not include a PPO contract. These Indemnity policies pay reasonable and customary charges only. Without a PPO contract included with your policy, a medical provider can balance bill you for charges above the reasonable and customary amount. For this reason we do not recommend purchasing Short Term Indemnity policies from Independence American or Companion Life.

Please also note: Non ACA-qualified Short Term health insurance plans are not required to cover certain “Essential Health Benefits” that are covered with ACA-qualified plans. These benefits are:

1.) Maternity and newborn care

2.) Mental health and substance use disorder services

3.) ACA mandated Preventive care benefits. However, routine mammograms, birth control and cancer screenings ARE COVERED with non ACA-qualified Short Term health insurance policies in states like Illinois where these Preventive care benefits are mandated.

4.) Pediatric Services (including both oral care and vision care).

The ACA (Obamacare) Individual Mandate was REPEALED by congress on 12/20/17. The Tax Cuts and Jobs Act of 2017 zeroed out the Individual Mandate on January 1, 2019.

2025 ACA open enrollment ended 01/15/2025. 2026 open enrollment begins 11/01/2025

Until November 1, 2025 you cannot purchase individual ACA-qualified health insurance unless you experience a Qualifying Life Event which will grant you a Special Enrollment Period. Depending on your total household A.G.I. – Adjusted Gross Income – you may qualify for one or both federal subsidies.

Depending on your total household M.A.G.I. – Modified Adjusted Gross Income – you may qualify for an A.P.T.C. – Advance Premium Tax Credit which will reduce your cost for health insurance. Advance Premium Tax Credits (federal health insurance subsidies) have increased significantly since April 1, 2021 due to the passage of the American Rescue Plan. Those enhanced subsidies have been extended until 2026 due to the passage of the I.R.A. – Inflation Reduction Act. Depending on your income, you may find a more affordable plan even if you earn a substantial income. To see if you qualify for a federal subsidy click here. You will be able to shop all carriers, choose a plan, get your subsidy and finish the process much faster than working solely with Healthcare.gov. You can also purchase ACA-qualified health insurance policies without subsidies using the same link if you do not qualify for Advance Premium Tax Credits.

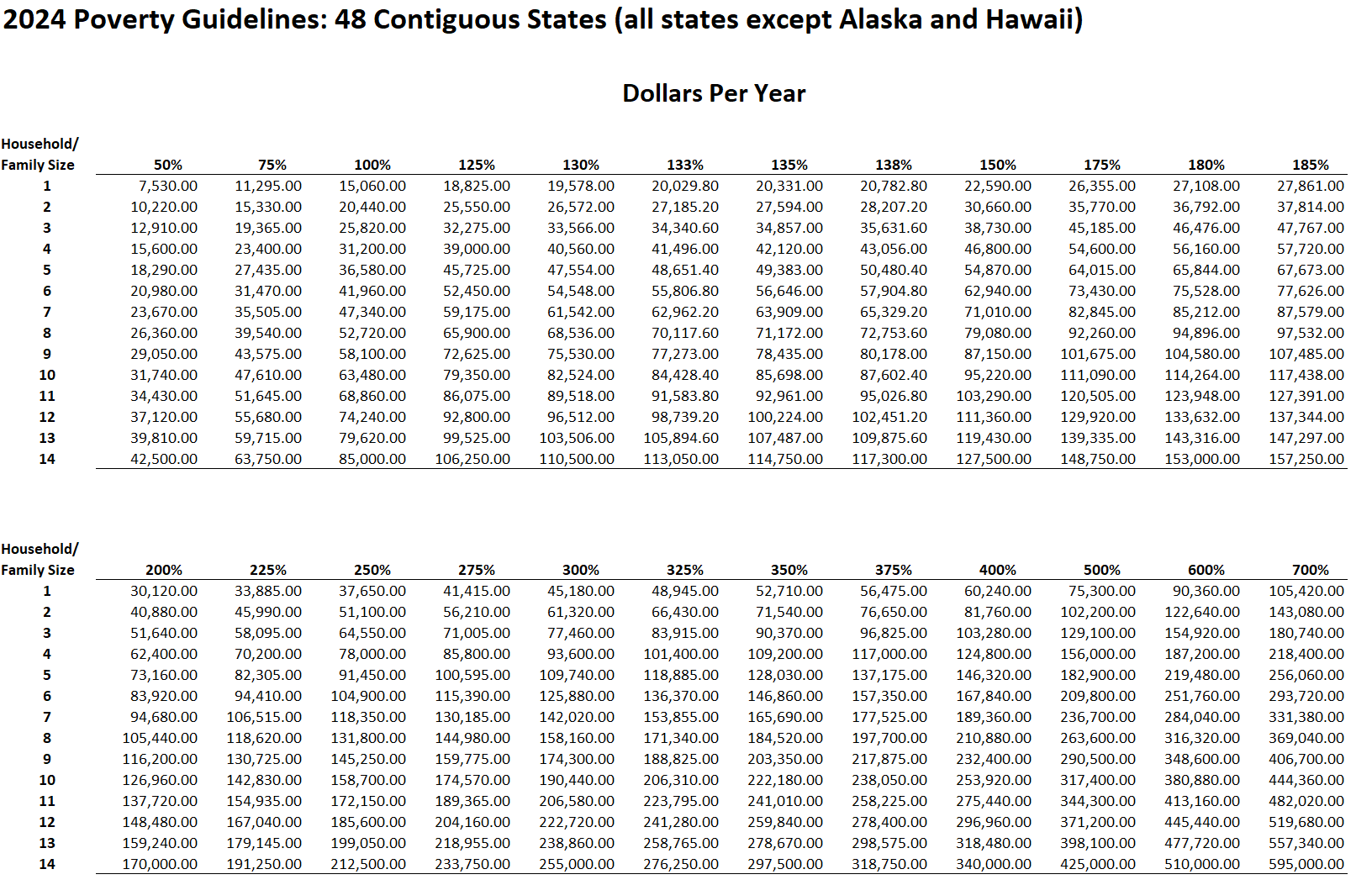

Please note: If your income is lower than the Federal Poverty Level Information in your state, which is less than 138% of the FPL – Federal Poverty Level in states that expanded Medicaid and less than 100% of the FPL in states that did not. You will be offered Medicaid and as such will not be able to qualify for subsidized private health insurance. You can purchase private health insurance even if you qualify for Medicaid but you must do so without a subsidy. Click the chart below to determine the current Federal Poverty Level and percentages above it.

Please note: If you qualify for a federal health insurance subsidy and your state has expanded CHIP – Children’s Health Insurance Plan – you may not be able to insure your children on your policy. Healthcare.gov will instead send a referral to your state’s CHIP program. In Illinois, that program is “All Kids Covered“. You may wish instead to purchase private health insurance at full price for your children if you cannot find a Pediatrician who will accept “All Kids Covered”.

Preventive Care: All ACA-qualified (Obamacare) health insurance policies must cover the following list of preventive services without charging you a copayment or coinsurance. This is true even if you haven’t met your health plan deductible. Click here to see the list. Be sure to click on “For all Adults”, “For Women” and “For Children” to see entire list.

Principal Broker, C. Steven Tucker joined Dan Proft and Amy Jacobson on Chicago’s Morning Answer to discuss the impact of the “Inflation Reduction Act” on Medicare Part D and enhanced ACA health insurance subsidies now extended until 2026 – 08/17/2022. Replay below: